WASHINGTON — The Federal Reserve on Wednesday enacted a quarter percentage point interest rate increase, expressing caution about the recent banking crisis and indicating that hikes are nearing an end.

Along with its ninth hike since March 2022, the rate-setting Federal Open Market Committee noted that future increases are not assured and will depend largely on incoming data.

“The Committee will closely monitor incoming information and assess the implications for monetary policy,” the FOMC’s post-meeting statement said. “The Committee anticipates that some additional policy firming may be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.“

That wording is a departure from previous statements which indicated “ongoing increases” would be appropriate to bring down inflation.

While comments Fed Chair Jerome Powell made during a news conference were taken to mean that the central bank may be nearing the end of its rate-hiking cycle, he qualified that the inflation fight isn’t over.

“The process of getting inflation back down to 2% has a long way to go and is likely to be bumpy,” the central bank leader said.

Also, Powell acknowledged that the recent events in the banking system were likely to result in tighter credit conditions, and that was likely why the central bank’s tone had softened.

Still, he said that despite market pricing to the contrary, “rate cuts are not in our base case” for the remainder of 2023.

Stocks initially rose after the Fed’s decision, but slumped following Powell’s remarks.

“The U.S. banking system is sound and resilient,” the committee said, in its prepared statement. “Recent developments are likely to result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring, and inflation. The extent of these effects is uncertain. The Committee remains highly attentive to inflation risks.”

During the news conference, Powell said the FOMC considered a pause in rate hikes in light of the banking crisis, but ultimately unanimously approved the decision to raise rates due to intermediate data on inflation and the strength of the labor market.

“We are committed to restoring price stability and all of the evidence says that the public has confidence that we will do so, that will bring inflation down to 2% over time. It is important that we sustain that confidence with our actions, as well as our words,” Powell said.

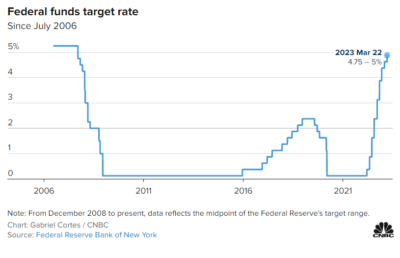

The increase takes the benchmark federal funds rate to a target range between 4.75%-5%. The rate sets what banks charge each other for overnight lending but feeds through to a multitude of consumer debt like mortgages, auto loans and credit cards.

Projections released along with the rate decision point to a peak rate of 5.1%, unchanged from the last estimate in December and indicative that a majority of officials expect only one more rate hike ahead.

Data released along with the statement shows that seven of the 18 Fed officials who submitted estimates for the “dot plot” see rates going higher than the 5.1% “terminal rate.“

The next two years’ worth of projections also showed considerable disagreement among members, reflected in a wide dispersion among the “dots.” Still, the median of the estimates points to a 0.8 percentage point reduction in rates in 2024 and 1.2 percentage points worth of cuts in 2025.

The statement eliminated all references to the impact of Russia’s invasion of Ukraine.

Markets had been closely watching the decision, which came with a higher degree of uncertainty than is typical for Fed moves.

Earlier this month, Powell had indicated the central bank may have to take a more aggressive path to tame inflation. But a fast-moving banking crisis thwarted any notion of a more hawkish move – and contributed to general market sentiment that the Fed will be cutting rates before the year comes to a close.

Estimates released Wednesday of where Federal Open Market Committee members see rates, inflation, unemployment and gross domestic product underscored the uncertainty for the policy path.

Officials also tweaked their economic projections. They slightly increased their expectations for inflation, with a 3.3% rate pegged for this year, compared with 3.1% in December. Unemployment was lowered a notch to 4.5%, while the outlook for GDP nudged down to 0.4%.

The estimates for the next two years were little changed, except the GDP projection for 2024 came down to 1.2% from 1.6% in December.

The forecasts come amid a volatile backdrop.

Despite the banking turmoil and volatile expectations around monetary policy, markets have held their ground. The Dow Jones Industrial Average is up some 2% over the past week, though the 10-year Treasury yield has risen about 20 basis points, or 0.2 percentage points, during the same period.

While late 2022 data had pointed to some softening in inflation, recent reports have been less encouraging.

The personal consumption expenditures price index, a favorite inflation gauge for the Fed, rose 0.6% in January and was up 5.4% from a year ago – 4.7% when stripping out food and energy. That’s well above the central bank’s 2% target, and the data prompted Powell on March 7 to warn that interest rates likely would rise more than expected.

But the banking issues have complicated the decision-making calculus as the Fed’s pace of tightening has contributed to liquidity problems.

Closures of Silicon Valley Bank and Signature Bank, and capital issues at Credit Suisse and First Republic, have raised concerns about the state of the industry.

While big banks are considered well capitalized, smaller institutions have faced liquidity crunches due to the rapidly rising interest rates that have made otherwise safe long-term investments lose value. Silicon Valley, for instance, had to sell bonds at a loss, triggering a crisis of confidence.

The Fed and other regulators stepped in with emergency measures that seem to have stemmed immediate funding concerns, but worries linger over how deep the damage is among regional banks.

At the same, recession concerns persist as the rate increases work their way through the economic plumbing.

An indicator that the New York Fed produces using the spread between 3-month and 10-year Treasurys put the chance of a contraction in the next 12 months at about 55% as of the end of February. The yield curve inversion has increased since then.

However, the Atlanta Fed’s GDP tracker puts first-quarter growth at 3.2%. Consumers continue to spend – though credit card usage is on the rise – and unemployment was at 3.6% while payroll growth has been brisk.

https://www.cnbc.com/2023/03/22/fed-rate-hike-decision-march-2023.html?distinct_id=LtacJMihkm&user_email=steve%40stevejulian.com